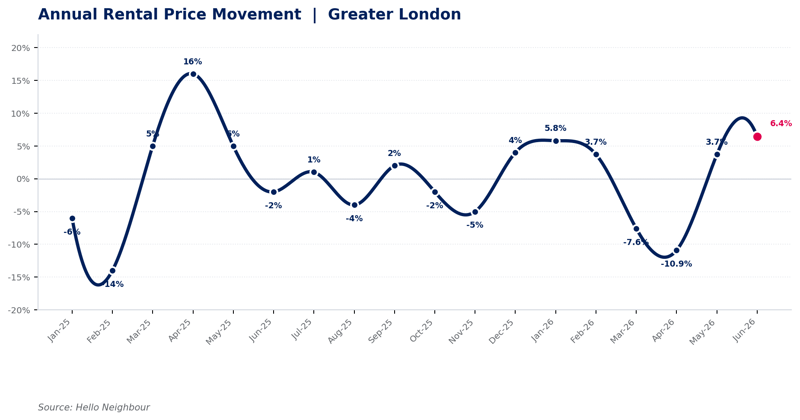

London rents rose 6.4% year on year in June, the third consecutive monthly increase and the strongest reading of 2026 so far. It is a clear step up from May's 3.7%, and it confirms that the sharp declines of early spring, down 7.6% in March and 10.9% in April, have well and truly steadied. That said, the headline deserves a note of caution: averaged across the last three months, rents are essentially flat, down around 1%. June points to a market that has found its footing rather than one embarking on a new upward run.

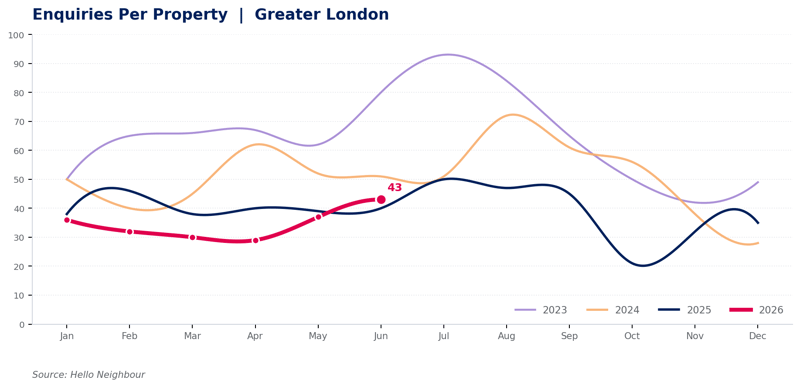

Demand climbs to its 2026 high.

Enquiries per property rose to 43 in June, up from 37 in May and the highest level we have recorded all year. The recovery that finally arrived in May has carried through, and June marks an important milestone: for the first time in 2026, demand has pushed clearly above the same month a year earlier.

For context, we recorded 40 enquiries per property in June 2025, 51 in June 2024 and 80 in June 2023. So while demand is now ahead of last year, it remains below the busier peaks of 2023 and 2024. What has not changed is how active London looks against the national backdrop. At 43 enquiries per property, the capital sits comfortably above the Rightmove average of around 12. For landlords, that means a healthy pool of interested tenants and real competition for well-presented, sensibly priced homes.

Demand Jun 26

The Renters' Rights Act and what it means for the data

The Renters' Rights Act has been in force since 1st May, and it continues to shape how these figures should be read. One of its most significant provisions for the lettings market is that landlords can no longer accept offers above the advertised asking price. Homes must be let at the rent they are listed at.

The likely knock-on effect is straightforward. With the option of accepting higher competing bids now removed, landlords have a clear incentive to advertise at a higher price from the start, to capture the level the market will bear. If enough landlords do this, advertised rents drift upward and the year-on-year percentage rises with them, without necessarily reflecting a real increase in what tenants were previously paying. June's stronger figure may carry some of this effect. It is still too early to separate it cleanly from genuine market movement, but it is firmly on our radar as the new rules settle in.

It is also worth remembering that the Act abolished the Assured Shorthold Tenancy. All new lets are now Assured Periodic Tenancies, and Section 21 no longer exists. Getting the right tenant in from the outset matters more than ever.

Affordability is still the anchor

Beneath the monthly movement, affordability remains the dominant force in the London market. Rents ran well ahead of tenant budgets over the previous two to three years, and we can see that impact coming through in the latest rental pricing.

The pattern on the ground reflects this clearly. Homes priced in line with current demand are letting quickly, often within days, while those anchored to last year's expectations sit longer and usually end up reducing. June's stronger headline does not change this dynamic. If anything, it reinforces the value of pricing accurately, because a higher advertised figure only works if it is grounded in what tenants will actually pay.

The wider national picture

June's London reading sits within a broader national rebalancing. Recent industry data has continued to point to cooling rental growth across the UK, with improving supply, steadier demand and a stronger route to first-time buying all easing the pressure that drove rents sharply higher in previous years.

London has, in effect, led this correction rather than lagged it, with the steepest adjustments concentrated at the new-let end of the market where rents had run furthest ahead of affordability. The steadier readings of May and June suggest the most acute phase of that correction may now be behind us. As ever, one quarter does not make a trend, and the new pricing rules add a fresh variable to watch.

What this means for landlords

A steadier market, demand at its highest of the year and a major regulatory shift all landing at once make this a moment for landlords to get the fundamentals right. Three things matter most.

Price realistically. Even with demand recovering, the cost of overpricing is significant. Every week a property sits empty is income lost, and that loss usually outweighs any premium a landlord hoped to achieve. With the new asking-price rules in force, setting the right figure from day one has never mattered more, because the advertised rent is now the rent.

Choose the right tenant. With Section 21 gone and every new let an Assured Periodic Tenancy, getting the right tenant in at the start is far more important than it used to be. Thorough referencing, fraud checks and a professional inventory are the foundation of a secure, low-stress tenancy, not optional extras.

Keep costs under control. Margins remain tight. Landlords paying high street agency fees, ongoing letting fees or marked-up maintenance charges are watching those costs eat directly into their yield. Reviewing what you pay to let and manage your property is one of the most effective ways to protect your return in the current market.

Our outlook for the rest of 2026

Our view is broadly unchanged. We expect rents to stay largely flat across the rest of the year, with month-to-month swings reflecting seasonal patterns and the new pricing rules rather than any sustained trend. Demand should hold up through the summer, likely staying ahead of 2025 but below the peaks of 2023 and 2024. The key variable to watch is how far the asking-price rules push advertised rents over the coming months, and how much of any future year-on-year rise reflects that rather than genuine underlying growth.

If you want to understand what all of this means for your specific property, our team is here to help you price accurately, find the right tenant and stay compliant with the new rules.

In Case You Missed It

A few other pieces from the Hello Neighbour blog this month that landlords may find useful. I found the landlord economics one fascinating. There is no real data out there on this that we could find, and although we all know landlord returns have been getting squeezed, it is only when you actually run the numbers that it becomes clear just how much:

COMMENT