Rising costs, flat rents and the Renters' Rights Act have squeezed UK landlord returns to around, and in most cases below, what a Cash ISA pays. We modelled eight worked examples across London and Manchester. Only one of them beats the ISA on income alone.

There is a great deal said about landlord economics, but very little of it adds up to a clear answer to the question landlords actually want to know: after everything, how much do I make on the capital I have tied up in this property?

So we ran the numbers. Hello Neighbour manages or supports nearly 1,000 properties, has let over 3,000 a year, and has handled around 4,000 maintenance jobs in the last year alone. We have used that data to model eight worked scenarios on real average properties in London and Manchester. We have looked at owning outright and owning with a 75% LTV mortgage, and at using a high-street agent or letting through Hello Neighbour's DIY platform.

What follows is the headline picture. The Renters' Rights Act arrives on 1 May 2026, mortgage rates have re-priced, and maintenance is up sharply. The economics have moved, and not in landlords' favour.

Why Return on Equity is the right measure

Gross yield is the number most landlords quote, but it ignores costs. Net yield is better but still measures returns against the full property value, which is misleading once a mortgage is involved.

The right comparator is Return on Equity (ROE): the cash return after all costs and tax, measured against the capital the landlord actually has tied up. For an unmortgaged property that is the full value. For a mortgaged property it is the equity stake, which is much smaller. ROE is the right number because it is what would otherwise be earning interest in a savings account if the landlord sold up. The benchmark we use throughout is the easy-access Cash ISA at 4.31% (April 2026): tax-free, no tenants, no risk.

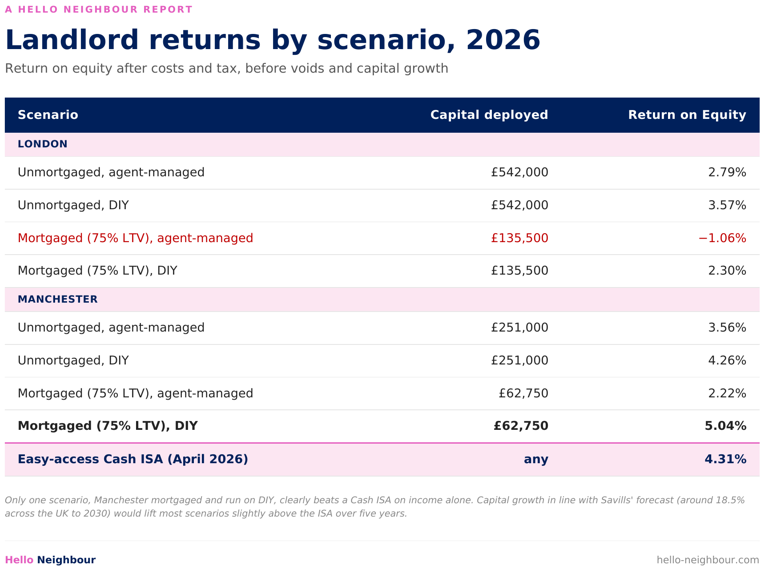

The headline result: only one scenario clearly works

The table below summarises what an average property in London or Manchester actually delivers on equity, before any house price growth, before voids, and on current 2026 cost and tax assumptions.

Only one scenario, Manchester mortgaged and run on DIY, clearly beats a Cash ISA on income alone. The London leveraged position run by an agent actually loses money each year. Most of the other scenarios sit somewhere between 2% and 4%: returns that compare poorly with a no-risk, no-tenant alternative.

This is before any capital growth. Capital growth in line with Savills' recent forecast (around 18.5% across the UK between 2026 and 2030) would lift overall returns slightly above the ISA over five years. But the income picture, year by year, is weak.

What has changed for landlords

Four things have moved against landlords at once.

1. Maintenance and repair costs are up sharply

Drawing on around 4,000 maintenance jobs across our portfolio over the last year, the average reactive repair cost is now £180 per job, with an average property generating just under five issues a year. That puts our portfolio average at around £1,000 per property per year. Independent data points higher: Towergate Insurance reported the average UK maintenance and repair cost at £1,374 per property in May 2025 (up 26.24% since 2022), and £3,197 in London. We have taken a conservative assumption of £1,500 in London and £1,000 outside London for this analysis.

Pegasus Insight reported that maintenance and repairs account for 31% to 39% of total landlord expenditure in early 2026. We covered this in detail in What Really Goes Wrong in a Rental Property, And How to Avoid It.

2. The Renters' Rights Act has added risk and cost

With Section 21 abolished and tenancies moving from fixed term to periodic, every problematic tenancy is now resolved through a slower, more expensive Section 8 court process. Three things have moved from optional to essential for any sensible landlord:

- Professional referencing with open-banking-based affordability checks (around £24 per person).

- An independent inventory at the start and end of every tenancy, assumed every three years (£95).

- Rent guarantee and legal expenses insurance (£250 a year).

Assuming a new tenant every three years, that adds around £300 per year to the cost base. Skipping these steps isn't saving money, it is accepting more risk in a market where the cost of getting it wrong has risen.

3. Mortgages have re-priced

The Bank of England base rate peaked at 5.25% in August 2023 and was held at 3.75% at the April 2026 MPC. Roughly 1.8 million fixed-rate buy-to-let deals were originally set to expire in 2026, many at pandemic-era rates of 1 to 2%. A typical leveraged landlord is moving from a rate near 2% to one near 5%, more than doubling monthly mortgage cost. For our examples we have used a 75% LTV interest-only buy-to-let at 5%.

4. Letting agent fees have stayed high

The high-street agent model still typically charges around 20.4% (including VAT) for a fully managed service in London, with lower fees outside London. That fee usually covers the agent's service only; safety certificates, inventory, referencing and insurance are still extras the landlord pays. The DIY alternative through Hello Neighbour Get Rented is £59 to find a tenant every three years, then around £20 a year of compliance and admin if landlords manage day-to-day themselves.

Two business models, two service routes

Strip away the complexity and there are two basic landlord business models: owning outright, or owning with a mortgage. The difference matters because the same property delivers very different returns on the capital actually deployed. A £100,000 equity stake earning £1,500 a year is a 1.5% yield on equity, not on property value.

Within each model there are two practical service routes:

- Route A: Pay a high-street agent to find a tenant and manage the property day-to-day.

- Route B: Find a tenant yourself through an online platform like Hello Neighbour and manage the property yourself, with the same compliance, contracts and insurance in place.

Both routes appear in every one of our eight examples. The DIY route consistently delivers a better return because the agent fee, often £5,354 a year on a London average property, is the single largest avoidable cost.

What the eight examples show

Across the eight scenarios, five clear patterns emerge.

Manchester DIY is the only scenario that clearly beats the ISA on income

At 5.04% ROE, the mortgaged Manchester landlord running their own property is the only example in the analysis to beat the 4.31% Cash ISA on income alone. They benefit from a higher gross yield (5.93%) than the mortgage rate (5%), so leverage works in their favour. Section 24 tax relief, restricted to a 20% credit on mortgage interest, exactly matches their tax band, so the relief is not punitive.

The leveraged London agent route loses money every year

At −1.06% ROE, the London landlord using a high-street agent and a 75% LTV mortgage runs an annual loss of around £1,440. Switch the same landlord to DIY and the position turns into a £3,115 profit, a £4,555 swing. The agent fee on a London property at 20.4% is the single biggest cost the landlord can choose not to pay. (The Section 24 mortgage-interest credit is capped at the tax actually payable, so on a pre-tax loss it cannot create a refund.)

Section 24 hits higher-rate landlords disproportionately

Mortgage interest is no longer fully deductible against rental income. Instead, landlords get a 20% tax credit on interest paid. For basic-rate taxpayers this matches the tax rate. For higher-rate (40%) or additional-rate (45%) taxpayers, it does not, and the effective tax burden is far higher.

Manchester beats London on yield

The numbers reflect what most landlords know: cheaper properties with comparable rents produce higher gross yields and therefore higher returns on equity. Across all four pairings, Manchester delivers a better ROE than London for the same model.

Managing the property yourself adds 0.8 to 2.8 percentage points

Across the four pairs, the DIY route adds between 0.8 and 2.8 percentage points of ROE compared with the agent route. The biggest gains are on leveraged properties where the agent fee is a much larger share of a smaller equity return.

Beyond the eight: regional and hotspot data

To pressure-test the headline finding, we ran the same analysis across Zoopla's regional rental data and the ten highest-yielding cities Zoopla identified in their September 2025 hotspots research. The picture is consistent.

Across the eleven UK regions, only Scotland and the North East deliver returns above a Cash ISA when an agent is used. Add DIY management and the picture broadens: the North West, Wales, Yorkshire and the Humber, and the West Midlands all rise above the ISA threshold.

The hotspots are a different story. All ten cities Zoopla identified, Sunderland, Aberdeen, Burnley, Dundee, Middlesbrough, Hull, Blackburn, Glasgow, Grimsby and Liverpool, deliver an above-ISA return. Sunderland tops the list at 7.66% on the agent route and 12.05% on DIY. The hotspots are real, but they represent a small fraction of the UK rental market.

Voids and capital growth

Our headline analysis assumes no void periods. In practice, even a well-run portfolio runs occasional voids. Each week of void costs around 2% of annual rent, plus continuing council tax, utilities and any service charge. We modelled the impact of a 21-day void once every three years. Only the Manchester mortgaged DIY scenario still beats the Cash ISA. The rest drop further below.

Capital growth is the other part of the equation. Savills' November 2026 forecast assumes a 2% decline in 2026, then 2.5%, 5%, 6% and 6% through to 2030, for a cumulative 18.5% across the UK. The London-specific Savills forecast is lower, at 10.6% over the same period. Knight Frank expects 1.5% in 2026, 3% in 2027 and 4% in 2028. Over five years, that capital growth would lift the overall return slightly above the Cash ISA for most of our scenarios, but the income picture remains weak.

For landlords thinking of buying a new property today, the maths is harsher. SDLT alone on a £542,000 London buy-to-let is £44,200, and total acquisition costs are around £49,675 before the keys turn. We model that in detail in the full report.

What landlords can do about it

The economics are tight, but the answer for most landlords is not to sell. It is to focus hard on costs, which is what many already do.

- Manage the property yourself where possible. The DIY route adds 0.8 to 2.8 percentage points of ROE compared with the agent route.

- Cut expensive reactive repairs through prevention. Boiler servicing, mould checks and small plumbing fixes head off the most expensive failures. See our maintenance data analysis for the patterns.

- Run a tight tenancy. Professional referencing, an independent inventory and rent guarantee insurance now pay for themselves by reducing the risk of a long, expensive Section 8 process under the new Act.

- Keep voids short. Mid-tenancy inspections, fast turnaround and good marketing all matter. We covered this in Why Property Inspections Are a Key Tool for Landlords.

- Check your licensing exposure. Selective licensing now applies to nearly 400,000 properties in England. Our Landlord's Guide to Property Licensing covers the detail.

How Hello Neighbour can help

We built Hello Neighbour to give landlords the tools to run a tenancy themselves at a fraction of the cost of a high-street agent, with the same compliance and the same legal protection.

Get Listed (£29): List on Rightmove, Zoopla and OnTheMarket. Find a tenant yourself.

Get Rented (£59): Everything in Get Listed plus payment collection, compliance, the tenancy contract and move-in. The DIY route in this analysis.

Property Management (from £102 per month): Fixed-fee, dedicated property manager, rolling contract, up to 60% less than a high-street agent.

Add-ons cover the items the Renters' Rights Act now makes essential: independent inventory (£95), tenant references (£24 per person), rent and legal protection (£250), gas safety, EICR and EPC certificates.

The bottom line

Landlords are not getting rich any time soon. The combination of higher costs, the Renters' Rights Act, re-priced mortgages and a flat rental market has compressed returns to a level where, on income alone, most scenarios sit at or below a Cash ISA.

The right response for most landlords is not to sell. It is to treat the property as a long-term capital play, with house price growth doing the heavy lifting over five years, and to be ruthless about costs in the meantime. The two biggest avoidable costs are the high-street agent fee and reactive repairs. Take control of both and the maths starts to work again.

If you would like the full 28-page Landlord Economics report with the worked examples, regional and hotspot tables, voids analysis and BTL appendix, you can donwload it here or get in touch at contact@hello-neighbour.com

COMMENT