It has never been more important to get the rent right. It is no longer just about maximising income. The Renters' Rights Act gives tenants the right to challenge rent that sits above open market level, and a Tribunal can only ever reduce it, not increase it. In addition, landlords can't accept an offer above their advertised rent, so under-pricing at the start can't be corrected later. So landlords have to get the rent right at the start and be able to prove that it is at an open market level if required.

Tenants can challenge any initial rent within 6 months of the start of a tenancy, even if they accept it at the start, and those challenges follow the more legalistic route of Tribunals.

Rent increases can also be challenged any time a landlord proposes one.

The process of challenge is unlikely to be quick, and even if a rent is accepted as open market it will only come into effect once the tribunal has ruled. That means valuations need clear, solid evidence, not opinion, and that means reliable data is at a premium.

It also means that the negotiation of a rent increase needs detailed supporting evidence, to hopefully avoid the tribunal altogether. Persuading a tenant that their chances of "winning" at tribunal are low is the real aim for landlords.

At Hello Neighbour we have let over 4,000 properties, we have done well over 10,000 viewings and collected feedback from each one. We have helped negotiate over 7,000 offers. We know what tenants are looking for and what drives value. But we still use a raft of external data to make sure that we provide the evidence landlords will need to justify rent levels in this new legal world.

A well thought through valuation report that is supported by a range of relevant data that is proven to impact value will stand up much better under legal scrutiny than just "gut".

Just ask for a free valuation and you will see the lengths Hello Neighbour goes to, in order to make sure landlords are as professional as they can be and have the best support for their rent level. If you want us to negotiate a rent increase and help you with the process, we can do that too.

In this article:

- Getting legal: why getting the valuation right matters more than ever

- First-tier Tribunals

- Wider market factors

- The regional picture: one market, many speeds

- Location, location, location

- Property factors: type, size, layout and condition

- Property features: what tenants actively look for

- Tenant factors: demographics, affordability and demand shifts

- How rental valuations are actually done

- What to do to maximise value

- Negotiating rent increases

- The real cost of overpricing

Getting legal: why getting the valuation right matters more than ever

Pricing a rental property accurately has always mattered, but the Renters' Rights Act has raised the stakes considerably. Since May 2026, landlords can only increase rent once a year, and only up to the open market rate, and if a tenant disputes the figure, you may have to justify it at the First-tier Tribunal with as much evidence as you can provide.

That cuts both ways. Set the rent too low and you simply leave money on the table for a full twelve months until you can revisit it. Set it too high and you risk extended voids, which erode returns far faster than a modest rent ever recovers. And if you push an increase above market and the tenant appeals, the existing rent can continue to apply until the First-tier Tribunal reaches a determination, with no backdating. So an over-ambitious figure can mean months with no uplift at all, and quite possibly a determination below what a defensible, market-based valuation would have achieved in the first place. In short, accurate valuation is no longer just good practice; it's the difference between protected income and avoidable loss.

The good news is that rental value isn't arbitrary. It's the outcome of overlapping factors; some fixed by the wider market, some by location, some by the property itself, and some by who your tenant is. Understanding which of those you can influence, and which you can only account for, is what separates confident pricing from guesswork. This guide works through them in turn.

First-tier Tribunals

The role of the Tribunal is to decide: "What is the open market rent that this property would achieve if it were let today on the open market?"

The Tribunal's own guidance says it will look at rents of similar properties in the local area. The Tribunal will ignore any improvements to the property made by the tenant to avoid inflating the rent.

The Tribunal needs as much detail as possible about your tenancy to make a decision, and there is guidance on the government website.

Although it is early days in terms of establishing precedent, it is likely the focus will be on comparable properties. Landlords may also decide to take legal advice.

It is of interest when considering rent levels that the tenant application form for the Tribunal includes the following:

- any floor plans; if not available, a rough layout will work

- a recent photo of each room, showing as much of the room as possible

- an outdoor photo of the front of the property

- the size of each room

- the property's features, such as central heating, double glazing, carpets, curtains, appliances and furnishings, including details of who provided them

- details and photos of any repairs or improvements that have been done, including who did the work and who paid for it

- local amenities, including nearby public transport, shops, schools or other conveniences

- any other documents that support their case

Wider market factors: you can't ignore the market you're operating in

No property is priced in a vacuum. The broadest driver of what you can achieve is the balance of supply and demand in the wider market, and right now that balance is shifting.

After several frantic years, Zoopla reports that rental growth has cooled to its slowest pace in around four years at roughly 2-3%. Supply has risen and demand has eased. The average UK rent now sits at about £1,350 a month. Hello Neighbour expects a broadly flat market for the remainder of the year.

The point for a landlord is that the macro climate sets the backdrop for confidence. A market with falling vacancy and rising average rents supports more assertive pricing; one where new stock is arriving faster than tenants supports caution. You can't control these conditions, but your pricing should reflect which of them you're operating in.

The regional picture: one market, many speeds

National headlines flatten a great deal of variation, and pricing against the wrong benchmark is a common, expensive mistake.

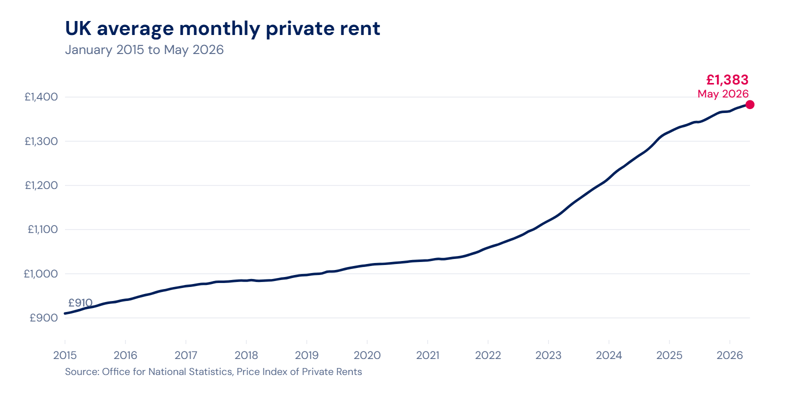

The ONS's official release covering the last 12 months to May 2026 shows how wide the gap can be. Average UK monthly rent is shown at £1,383, up 3.3%. England is at £1,442, up 3.4%, Wales at £836, up 4.7%, and in Scotland the average level is £1,009, up 1.0%.

In England, private rent annual inflation was highest in the North East (5.9%), and lowest in London (2.0%), in the 12 months to May 2026.

The takeaway is simple: the right comparator is local and must be current. A growth rate that holds in one region can be several points wrong a few hundred miles away.

Location, location, location: tenants look for lived convenience

Location is the most durable driver of rental value, but its influence is more specific than a town or a postcode. What tenants pay for is lived convenience: proximity to employment, transport, schools, shops and green space, relative to their income and how they prefer to live. Two streets in the same postcode can command meaningfully different rents if one sits closer to a station or inside a better school catchment.

A few location factors are worth isolating, because the data on each is clear:

Transport

Transport and connectivity remain a consistent source of premium wherever commuting matters. Walkable distance to a station or major bus corridor is observable in market data, with closer properties achieving higher rents than otherwise identical ones further away. Flexible working has softened this for some tenant segments without removing it.

Proximity to good transport remains one of the most reliably evidenced drivers of rental value, and one where the rent-specific data is unusually strong. Nationwide's controlled analysis (which strips out property type, size and neighbourhood) found a home 500m from a station commands around a 10.5% premium in London, though far less outside it (about 4.9% in Manchester).

On the rental side, JLL found average rental growth across London's Elizabeth Line reached 13.3%, ahead of every region it passes through, with 70% of station areas seeing rent growth above 10%. The effect on rents is often sharper than on prices: JLL notes that capital values tend to be "priced in" during construction, while the rental premium arrives after opening, as tenants pay immediately for the improved connectivity.

In JLL's tenant survey, 92% rated proximity to transport important, and 67% would pay more for it. The premium rewards convenient access rather than being directly on top of a line. Adjacency to a busy terminus can carry a noise penalty.

School proximity

Proximity to sought-after schools is one of the most consistent location premiums in the UK market, though the hard evidence is strongest for sale prices: ONS analysis found homes in the catchment of the top 10% of primary schools were around 8% more expensive than comparable homes further away, and 6.8% for secondary schools. The effect is highly regional; larger in London and the South East, often 3-6% across the North and Midlands, and it crucially depends on falling inside the current admissions boundary, not mere walking distance. In the rental market the signal is softer but real: agents report catchment demand can lift rents roughly 5-10% above local averages, as some families rent to secure a qualifying address.

Broadband

Good broadband and a usable home-office space have become genuine counterweights to transport for tenants who value connectivity over commuting distance, but both factors are obviously very tenant specific. Fast, reliable broadband has become a baseline expectation rather than a bonus; Rightmove considers it important enough to display predicted speeds on every listing. Previous studies have found broadband details ranked as a more important search feature than transport links and nearby schools.

Green space

Green space is a recognised, measurable contributor. ONS analysis of more than a million transactions, drawn from Zoopla data, found homes within 100 metres of public green space were on average around £2,500, or about 1.1%, more expensive than equivalent homes more than 500 metres away. In dense urban markets where private gardens are scarce the effect is far larger: Savills has found homes within 100 metres of an inner-London park or common command around a 15% premium. The closer the green space and the larger the area accessible, the stronger the effect, and the premium is most pronounced in urban locations where private outdoor space is scarce.

Local crime levels

Crime, and the perception of it, is a well-established downward influence on value, with "visible" crime that signals neighbourhood neglect tending to weigh more heavily than concealed offences. UK research published in Urban Studies found that each additional case of anti-social behaviour per ten people on a street is associated with roughly a 0.6-0.8% fall in property prices, with violent crime reducing prices by around 0.6-1.6%. The effect is strongly local, so values are best assessed against street and neighbourhood-level crime data rather than wider district averages.

Social renting

The local tenure mix is more nuanced than it's often assumed to be. A high concentration of social rent is sometimes treated as a simple discount, but UK research from the NHBC Foundation found that well-integrated, good-quality social housing does not reduce surrounding values. What correlates with weaker values is concentration, which usually acts as a proxy for wider area deprivation rather than a cause in itself. Use it alongside crime and deprivation data, not as a standalone adjustment.

Regeneration

Finally, regeneration is the location factor most worth watching over a three-to-five-year horizon, though the hard evidence is strongest for sale prices: CBRE found homes within 750 metres of major London regeneration schemes saw an average annual price premium of around 3.6% versus the wider local authority, rising to 5-7.6% in standout cases like Stratford and Woolwich. The rental effect is harder to isolate cleanly, but it's real, as the new transport links and jobs that regeneration brings take effect. Agents report notably stronger rent growth in regenerating, well-connected areas such as East London's Elizabeth Line corridor. The premium builds over time, typically becoming tangible once early residents and amenities arrive rather than at announcement.

Property factors: type, size, layout and condition

Property type sets the broadest parameters: a flat competes with flats, a house with houses, an HMO in a different segment entirely. Within each type, bedroom count drives the headline figure, but layout efficiency often matters more than raw floor area. A two-bedroom property with genuine double bedrooms, a practical kitchen and real storage will out-let a technically larger home with a cramped layout.

From our own viewings feedback we know that size and layout dominate, with size, kitchen and storage representing more than half the negative comments. There's more in Finding the Right Tenant: Hello Neighbour's guide to viewings.

Condition and presentation is the most controllable short-term driver, and the most commonly underestimated. Tenants form rapid impressions from décor, flooring, and the state of the kitchen and bathroom. A well-presented property at the midpoint of the local market lets faster and attracts stronger applicants than a poorly presented one at the same price. Dated bathrooms, worn flooring and years without redecoration will suppress achievable rent regardless of how strong the area is.

Furnishing level should match the target tenant, not the landlord's instinct. Furnished commands a modest premium in high-turnover city-centre markets among young professionals; in areas dominated by longer-staying families, unfurnished is the expectation and furniture adds cost without adding rent.

Property features: what tenants actively look for

Beyond the structure, specific features will impact demand. A January 2026 survey of 2,000 UK renters by CIA Landlords puts numbers on long-standing portal search trends from Zoopla and Rightmove. The headline findings:

Affordability comes first

81% of renters rank rent affordability as a top or high priority, and the single biggest landlord deal-breaker is rent shocks, cited by 55%. Encouragingly, 81% say they'd stay five years or more in a home that met their priorities. A powerful argument for pricing sustainably rather than aggressively.

Energy efficiency

79% say a good EPC matters. The reason is concrete: Hamptons research shows a tenant in an average EPC C home pays roughly £499 a year less in bills than one in an EPC D, rising to about £1,248 versus an EPC E. That feeds straight into tenant affordability.

The Mortgage Works' 2026 analysis found an A/B-rated property attracts a rental premium of around 8.1% over a comparable D-rated home.

Outdoor space is a wellbeing issue, not a luxury

74% rate a private garden or access to outdoor space as important. It connects to the finding that 87% of renters say where they live matters to their mental wellbeing.

Parking and pets matter

Zoopla's keyword data has long shown parking and a garage near the top of renters' searches, and "pets" has climbed into the top three most-searched features in every region.

Other features that consistently earn their keep are ample storage, modern kitchens and bathrooms, good natural light, reliable fitted appliances, and basic security (solid locks, video doorbells, well-lit exteriors). The common thread is liveability, with tenants increasingly choosing a home they can settle into, not just somewhere to sleep.

Tenant factors: demographics, affordability and demand shifts

Every rental market has an affordability ceiling set by the income profile of its tenants. Demand above that ceiling is thin regardless of quality, so pricing above what the local tenant pool can afford produces either voids or over-extended tenants and avoidable arrears risk. Knowing your demographic isn't soft information; it's a strong contributor to realistic pricing.

And that demographic is changing in ways that reshape demand. The private rented sector is now the second-largest tenure in England with 4.7 million households, around 11 million people, roughly 19% of all households, but its make-up has shifted. Families with dependent children now account for around a third of private renting households, up sharply since the early 2000s. The average first-time-buyer age has risen significantly, and ONS projections point to continued growth in renting among older age groups. Many have adapted to renting as a settled status rather than a stepping stone.

This shows up directly in demand: Rightmove reports that searches for three and four bedroom rental homes have grown faster than searches for one-bedroom flats over the past five years, and with hybrid working embedded, family renters are increasingly looking beyond inner-city zones into the commuter belt and suburbs. The supply side hasn't kept up, with a landlord base still weighted towards smaller flats from the 2000s buy-to-let boom. So well-located, family-sized homes remain structurally scarce in many markets, and that scarcity is showing up in stronger rent growth for larger homes.

How rental valuations are actually done

When a letting agent or surveyor values a property, they're estimating what it would realistically achieve on the open market today. A few methods sit behind that figure, and it's worth understanding them. This is important because a First-tier Tribunal will expect a defensible basis if an increase is challenged.

The workhorse for residential lettings is Comparative Market Analysis: comparing the property against similar homes recently let or currently available nearby, then adjusting for differences in size, condition and features. It's market-driven and grounded in real evidence, which is exactly what a First-tier Tribunal wants to see. Its main limitation is finding genuinely comparable properties in thin or unusual markets.

For investment appraisal rather than rent-setting, investors also use yield-based and income measures. Rental yield (annual rent as a percentage of property value) is the headline return metric used. The Gross Rent Multiplier (price divided by annual gross rent) gives a quick comparison between properties. At Hello Neighbour we prefer more sophisticated approaches: the capitalisation rate (net operating income over value) and discounted cash flow (projecting and discounting future income) fold in operating costs, voids and the time value of money, and matter most when comparing investments or modelling a purchase.

For day-to-day rent-setting under the new regime, the practical message is that your asking rent should be evidence-based and documented. Keep all the information you have used, including the comparables and how you used them to come up with a figure, and make sure repairs and compliance are current before any review.

That turns a number into a defensible valuation.

What to do to maximise value

Not every improvement translates into higher rent. The ones that reliably do share a logic: they cut tenants' running costs, fix a functional deficiency, or align the property with what the local tenant pool actually expects. The ones that usually don't are luxury finishes above local market expectations, over-customised décor, and features a particular landlord values but the demographic doesn't.

In practice, the highest-return moves tend to be:

Invest in energy efficiency

It supports rent, cuts tenant bills, reduces voids, and is unavoidable anyway with EPC C required by 2030. It is one of the best-returning upgrades in most property types.

Refresh tired kitchens and bathrooms

Keep décor neutral and clean. Presentation drives first impressions and achievable rent more than almost anything else you can change quickly.

Add or formalise the features tenants search for

Usable outdoor space, parking, good broadband, a pet-friendly policy, and genuine storage. These are often low-cost relative to the demand they unlock.

Match furnishing to your target tenant

Rather than over or under-equipping by default, think about who the natural tenants are and how they will think about the property. It is dangerous to generalise too much, but for example: older tenants aiming for longer stays might prefer unfurnished, while younger, shorter-term tenants might be more mobile and so want furnished and functional.

Price against current, local comparables, and time your launch

Demand peaks in March to August and softens in the fourth quarter, and overpricing at launch tends to suppress the final agreed rent rather than protect it. A property sitting unlet for three or four weeks reads as "problem" to applicants and weakens your negotiating position. Practicality will often dictate the timing, but think about what the timing of your let means for seasonal demand.

Manage professionally

Responsive, compliant management attracts stronger applicants and reduces turnover. Tenants are paying for a service as much as a space, and lower turnover protects income as effectively as a higher headline rent. Start the tenant find as professionally as you can and continue your relationship with the tenant in the same way.

Get these right and you're not just chasing the market rent; you're presenting a property tenants actively want, which is what protects both the rent and the void periods over the long run. Under the Renters' Rights Act, where every increase has to stand up as open market rent, that defensible, evidence-led approach to value is no longer optional. It's the foundation of a profitable tenancy.

Negotiating rent increases

The very best result when negotiating an increase in rent is that you reach a level that the tenant will accept. Avoiding First-tier Tribunal delays and costs is a real win for your returns.

Approach the discussion in as professional a way as possible. That means having a detailed rationale for the increase based on all the evidence discussed above. Specifics and data count. Ultimately you need to persuade the tenant that the chances of a successful appeal to a First-tier Tribunal are slim.

Think about the overall returns to you. Pushing for a higher rent at the cost of significant voids will damage returns. Going too low will do the same.

The real cost of overpricing

The table below shows just how quickly a void period wipes out the benefit of a higher rent. With rent growth currently at around 3%, it takes just 11 days of vacancy to cancel out a full year's increase.

As an example, a 3% increase on a £2,000 per month property equates to an additional £720 in rental income per year. The daily rent on £2,000 is £67, so if vacant for 11 days that is £733 of rental income not received.

| Monthly rent | +15% | +10% | +5% | +3% (current) |

|---|---|---|---|---|

| £1,000 | £1,800 | £1,200 | £600 | £360 |

| £1,500 | £2,700 | £1,800 | £900 | £540 |

| £2,000 | £3,600 | £2,400 | £1,200 | £720 |

| £2,500 | £4,500 | £3,000 | £1,500 | £900 |

| Void days to wipe out gain | 54 days | 36 days | 18 days | 11 days |

The message is clear: with justifiable rent increases likely to be small in this market, it doesn't take much of a void period for landlords to start losing money, even if they ultimately achieve a higher rent.

Want a defensible number for your property? Ask for a free valuation.

Sources: Office for National Statistics (Private rent and house prices UK, Price Index of Private Rents, urban green space valuation, household projections); Zoopla rental market reports and keyword search analysis; Rightmove portal and survey data; English Housing Survey 2024-25; CIA Landlords / OnePoll renter survey (January 2026); The Mortgage Works buy-to-let energy efficiency analysis 2026; Hamptons; Savills; JLL; Nationwide; CBRE; NHBC Foundation; and peer-reviewed hedonic pricing research. Figures are indicative and were accurate at the time of writing. This article is general guidance, not legal or financial advice.

COMMENT